When we talk about fixed-income instruments, Treasury Bills (T-Bills) often come up, but many people don’t fully understand how they work or how to buy them. The good news is, T-Bills are one of the most accessible ways to grow your money with minimal risk, even if you’re starting small.

What Are Treasury Bills (T-Bills)?

Treasury Bills are short-term debt instruments issued by the Debt Management Office (DMO) through the Central Bank of Nigeria (CBN). They are essentially a way for the government to borrow money from the public for a fixed period — usually 91 days, 182 days, or 364 days — while offering you interest in return.

Here’s the key part: T-Bills are sold at a discount to their face value.

• You pay less than the face value when you buy.

• At maturity, you are paid the face value.

• The difference is your profit (interest).

Example:

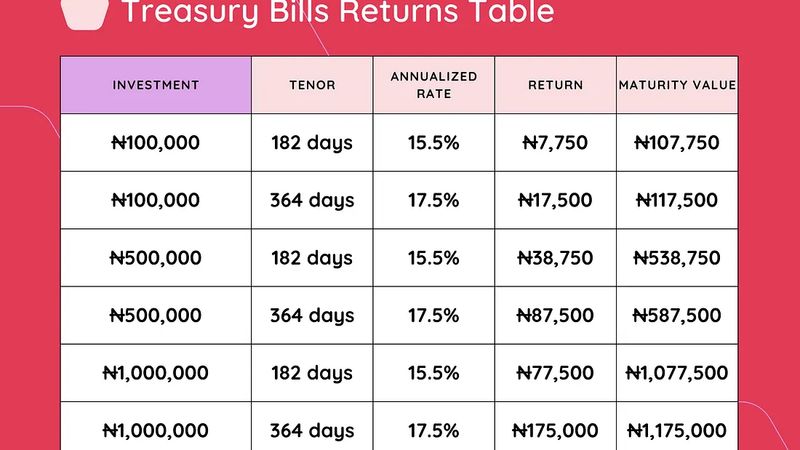

Let’s say you want to invest ₦500,000 in a 364-day Treasury Bill with a 15% annual rate.

• You won’t pay ₦500,000 upfront. Instead, you’ll pay about ₦425,000

• At maturity, you’ll receive the full ₦500,000 back.

• Your profit is: ₦500,000 — ₦425,000 = ₦75,000

This makes T-Bills different from fixed deposits, where you invest the full sum and earn interest on the face value at maturity. With T-Bills, the interest is essentially “front-loaded” through the discounted purchase price.

Where and How to Buy Treasury Bills in Nigeria

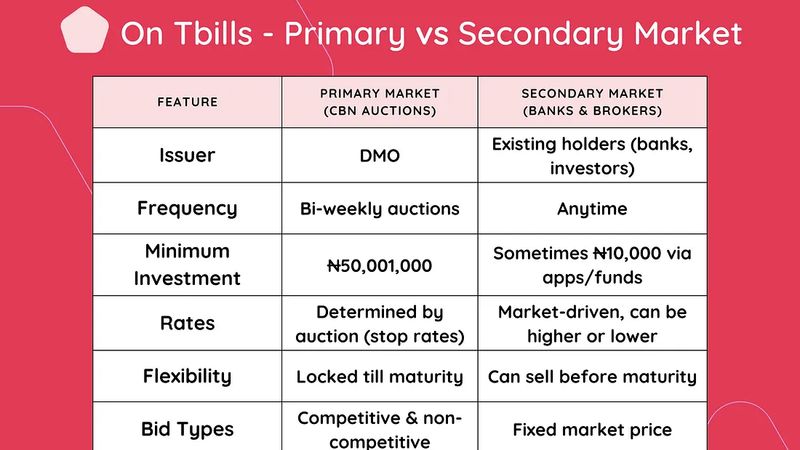

There are two main ways to buy Treasury Bills: Primary Market and Secondary Market.

1. Primary Market (Direct from DMO Auctions)

The primary market is where T-Bills are first issued by the DMO through bi-weekly auctions.

• Minimum amount: ₦50,001,000 (in multiples of ₦1,000).

• How to access:

1. Visit your bank (commercial or merchant bank).

2. Instruct them to bid for you at the auction.

3. Indicate your bid rate (competitive bid) or accept whatever rate is set (non-competitive bid). If successful, your account will be debited, and you will receive an investment certificate from your bank.

2. Secondary Market (through Banks & Brokers)

The secondary market is where you can buy already-issued T-Bills from banks, dealers, or brokers like Vetiva

• Minimum amount: Often from ₦10,000 (varies by institution).

• Flexibility: You don’t have to wait for auction dates.

• Rates: Slightly lower than primary market because dealers add a margin.

• How to access: Walk into your bank or use investment platforms that trade fixed-income instruments.

Expected Returns and Duration

Treasury Bills come in fixed tenors: 91 days, 182 days, and 364 days.

• Short-term (91 days): Lower interest, ideal for quick savings.

• Medium-term (182 days): Balanced returns and liquidity.

• Long-term (364 days): Higher returns, best for patient investors.

Current Yields

Rates fluctuate depending on government demand and economic conditions. Recently, yields have ranged between 14% to 20% per annum.

Tip: The longer the tenor, the higher the potential yield.

Primary vs. Secondary Market: What’s the Difference?

Risks and Limitations of Treasury Bills

Even though Treasury Bills are considered safe and low-risk, there are some limitations you should be aware of:

1. Inflation Risk

If inflation is higher than your T-Bill yield, your real return may be negative. For example, if inflation is 18% and your T-Bill yields 12%, your money is technically losing value in terms of purchasing power.

2. Opportunity Cost

T-Bills are safe, but they offer lower returns compared to riskier investments like stocks, mutual funds, or real estate. By locking money into T-Bills, you may miss out on higher-growth opportunities.

3. Liquidity Constraints

While you can sell T-Bills in the secondary market before maturity, it isn’t always easy or favourable. Prices may be lower if market conditions aren’t right, which can reduce your profit.

4. Fixed Returns

Unlike other investments, once you buy T-Bills, your return is locked in. If interest rates rise afterwards, you can’t take advantage until your T-Bill matures.

Why You Should Consider Treasury Bills

• Low Risk — Backed by the Federal Government.

• Predictable Returns — You know exactly what you’ll earn at maturity.

• Flexible Tenors — Choose between 3 months and 1 year.

• Liquidity — Can be sold before maturity in the secondary market if you need cash.

Treasury Bills are a great entry point for Nigerians new to investing. T-Bills allow you to earn steady returns without losing sleep over market risks.

Start small, understand the process, and gradually grow your investment portfolio. If you want even better results, consider mixing T-Bills with other assets like bonds, mutual funds, or stocks.